Trying to save for a childs post-secondary education can be tricky, especially because tuition, books, housing, and a few other education costs keep moving up. The Canada Education Savings Grant (CESG) 2026 does help in this area though, by letting families grow education savings through government support, paid into a child’s Registered Education Savings Plan (RESP).

The CESG is one of Canadas more valuable education savings tools, because it rewards families for planning ahead. When you put money into an RESP, many eligible households can receive extra funds from the federal government, and that extra boost helps the savings grow more quickly as the years pass.

In this guide, you will see most of what you need to know about the Canada Education Savings Grant (CESG) 2026. That includes who qualifies, contribution expectations, the grant amounts, yearly payment limits, and ways to stretch the benefits as much as possible.

What Is the Canada Education Savings Grant (CESG)?

The Canada Education Savings Grant CESG is a federal program that assists parents guardians, and other family members in saving for a child ’s post secondary schooling

If you put money into an RESP then the Government of Canada may attach a grant to your deposits, depending on how much you contribute.

So your education savings can keep growing thanks to:

- Contributions you make

- Federal matching or grants

- Earnings from investing

The CESG is run through eligible RESPs and it is open for children who meet the requirements under Canadian rules

What Is an RESP?

An RESP, meaning Registered Education Savings Plan, is a tax advantaged savings account made to support households saving for schooling costs

Funds inside the RESP can later be used toward:

- College tuition

- University tuition

- Trade school programs

- Apprenticeship courses

- Books and supplies

- Day to day living costs while studying

The CESG money is deposited directly into the child’s RESP account

Why is the CESG such an issue?

The price of getting higher education keeps rising.

Lots of families are up against serious costs, like

- Tuition fees,

- Textbooks

- Housing

- Transportation

- Technology

- Day to day living costs

The CESG eases some of that pressure by adding government contributions.

And because it is grant money, it generally does not need to be paid back, assuming the funds are used following the program rules.

Who can get the CESG in 2026

For the Canada Education Savings Grant in 2026, the child usually needs to:

- Be a resident of Canada

- Have a valid Social Insurance Number SIN

- Be listed as the beneficiary of an RESP

The RESP might be opened by

- a parent,

- a grandparent

- a legal guardian

- or another eligible subscriber

Also the RESP has to be set up through a participating financial institution

How Much Does the CESG Pay in 2026?

The federal government usually adds to a portion of what you put into your RESP each year , so there is a match.

The basic CESG works like this:

20% on the first annual contribution amount, up to the eligible limit .

For instance:

- If you contribute $2,500 to an RESP this year,

- Your contribution is $2,500

- Basic CESG comes to $500

So, that extra government support can quietly raise the value of long-term education savings.

Extra CESG for Lower and Middle Income Families

Some households may qualify for extra CESG support depending on income in the household.

Qualified families may get:

Higher grant percentages applied to part of the yearly contributions

- Extra government help in addition to the basic grant

- Income cutoffs and eligibility rules are reviewed from time to time .

Families should confirm the latest CRA and Government of Canada guidance before planning RESP contributions .

What Is the Highest CESG Amount a Child Can Get?

There is a lifetime grant cap for each beneficiary.

Once a child hits the maximum allowable CESG, no more grant deposits will be made into the RESP.

Because of that cap, several families begin contributing early, so the long-term growth can stretch as far as possible.

Can You Recover CESG for Missed Years?

Yes.

Many parents worry, when they did not set up an RESP right after the child was born.

Good news, there are catch-up rules that let families reclaim some unused CESG room.

You can receive grants through a mix of:

- Contributions made in the current year

- Some unused grant capacity from earlier years

This setup supports families who start saving later and still receive government help.

When Should You Begin an RESP?

In general, start sooner rather than later.

Early contributions usually give you:

- More chances to receive grants

- More investment growth time

- Bigger compound returns

- Less financial stress in the future

Even these modest monthly contributions can grow a lot over many years, with time doing most of the work.

How Can the CESG Assist Education Savings to Grow?

The CESG boosts the money going into the RESP.

For example:

A family makes payments of

- $2,500 each year

The government adds

- $500 as CESG each year

Over time, growth from the investments can apply to both the family’s deposits and the grant funds.

That combination may end up creating meaningful education savings, by the time the child begins post-secondary studies.

What Expenses can RESP Money Cover?

When the beneficiary gets enrolled in an eligible post secondary program, the RESP funds can, in most cases, help pay for a few categories that feel really practical.

Tuition

Tuition is often the biggest education cost.

Using RESP funds can reduce how much the student needs to rely on student loans.

Books and Supplies

Students often need things like:

Textbooks, Software, lab materials , and study resources.

RESP withdrawals can be used to pay for these kinds of costs too.

Housing

Many students end up living in one of these arrangements:

On campus, off campus, or away from home.

Housing can take up a large piece of the total budget.

Transportation

Education related travel and transport may include:

Public transit, travel between home and school, and vehicle related costs.

RESP funds can provide flexibility for this, especially when plans change.

What Happens if the Child Does Not Attend College or University?

Many parents worry about that scenario.

Fortunately, there can be several options.

Depending on the circumstances, the beneficiary might go into another eligible program. Or maybe a different eligible beneficiary can be named instead. In some cases certain funds can be moved according to RESP rules, and there may be other withdrawal choices too. Because every family situation is different, families should read the RESP rules carefully before making any call.

Can Grandparents Open an RESP?

Yes.

Grandparents often add money toward a grandchild education savings plan.

Opening an RESP may let grandparents:

- Make contributions

- Support receiving CESG payments

- Help cover future education costs

Lots of families treat RESPs as part of multigenerational financial planning.

Can More Than One Person Contribute?

Yes.

RESP contributions can come from Parents, Grandparents, Relatives, or Friends.

That said, contribution limits still apply to the beneficiary.

Families should coordinate contributions to avoid exceeding allowable limits.

How to Apply for the CESG

The application process is usually plain and straightforward, but people still stumble a bit.

Step 1: Get a SIN for the Child

A valid Social Insurance Number is needed.

Step 2: Start an RESP

Pick a participating financial institution that offers RESPs.

Possible choices are:

- Banks

- Credit unions

- Investment firms

- Financial advisors

Step 3: Fill in the Grant Forms

Most financial institutions will hand you the CESG paperwork when you open the RESP.

Step 4: Add Contributions

After money is put into the RESP, the eligible grant amounts can be added automatically.

Common CESG Mistakes to Avoid

Lots of families miss good chances because of avoidable errors.

Starting Too Late

If you delay RESP contributions, you can end up with:

- missed grant opportunities

- less investment growth

- reduced education savings

Forgetting to Get a SIN

If you do not have a valid SIN, CESG payments cant be processed.

Ignoring Contribution Planning

Smart contribution timing can help maximize grant eligibility, and that matters a lot for families.

Make sure you understand the yearly and lifetime limits too.

Not Checking RESP Statements

Looking over RESP statements regularly can help confirm:

- investment performance stays on track

- contributions get recorded accurately

- CESG payments are actually received

How the CESG slots into a familys financial plan

The CESG is only one fragment, of a bigger financial game plan, that continues over time.

Families should also keep in mind things like

- Emergency savings

- Retirement planning

- Tax credits

- Government benefits

- Child related assistance programs

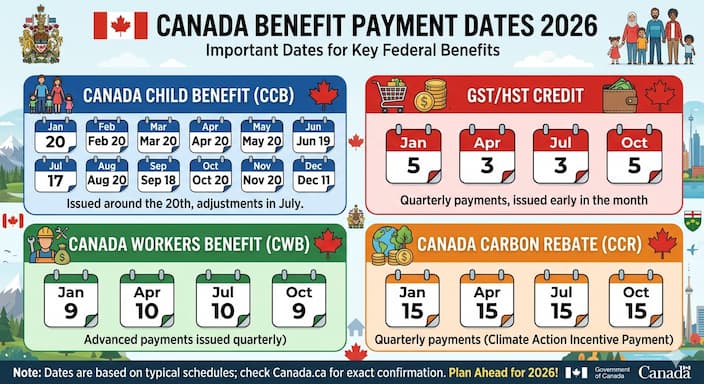

Parents receiving the Canada Child Benefit Payment Dates 2026 may choose to allocate a portion of those tax-free payments toward RESP contributions to help build future education savings.

Other Government Benefits Families Should Know About

Families saving for education may also qualify for additional government programs.

Canada Child Benefit (CCB)

The Canada Child Benefit provides monthly tax-free payments to eligible families raising children.

For payment schedules and eligibility details, see our Canada Child Benefit Payment Dates 2026 guide.

GST/HST Credit

Many families qualify for quarterly GST/HST Credit payments.

Our Canada GST/HST Credit Payment Dates 2026 article explains eligibility and payment schedules.

Canada Child Disability Benefit

Families caring for children with disabilities may qualify for additional support.

Learn more in our Canada Child Disability Benefit 2026 guide.

Alberta Child and Family Benefit

Families living in Alberta may qualify for provincial financial assistance.

Our Alberta Child and Family Benefit 2026 guide explains payment dates, eligibility requirements, and benefit amounts.

Frequently Asked Questions

Is the CESG Free Money

The CESG is a government grant that gets deposited into an RESP once eligible deposits have been made.

Families do not usually need to repay the grant if everything is used within the program requirements.

Do I Need an RESP to Receive CESG

Yes.

The CESG is only accessible through a Registered Education Savings Plan that qualifies.

Can Grandparents Receive CESG

Yes, grandparents can set up an RESP or contribute to one, and the eligible contributions could unlock CESG payments.

Can I Catch Up on Missed CESG Payments

Yes.

Many households can recover unused grant room by doing catch-up contributions.

Does Family Income Affect CESG

In some cases. Certain families may qualify for increased CESG support depending on household income.

Final Thoughts

The Canada Education Savings Grant (CESG) 2026 is still, in many ways, one of the best options for Canadian families looking to plan a childs education later on. If you put money into an RESP , families can receive government grant funding, experience long term investment growth, and end up needing less student debt.

Getting started early, adding funds on a steady basis, and understanding the grant guidelines, can help stretch education savings over the years. No matter if you are a parent, grandparent, or legal guardian, the CESG presents a solid chance to place resources into a childs future and make post secondary learning more reachable for everyone involved.